What is VAMP and why it matters

VAMP is Visa’s enforcement framework for fraud and dispute performance, designed to hold acquirers and their partners accountable. The Visa Acquirer Monitoring Program identifies merchants generating excessive fraud or disputes and places responsibility squarely on the providers that support them. Every dollar lost to fraud triggers a much larger drain, often times merchants lose nearly 5x for every dollar of fraud. VAMP combines fraud and disputes into a single ratio, increasing how quickly merchants and portfolios reach enforcement thresholds.

Fraud and disputes are treated as measurable risk, not isolated events.

Accountability extends to resellers, not just merchants.

Performance thresholds are defined and enforced by Visa.

Ongoing oversight replaces one time reviews.

Failure to manage risk becomes a network issue, not an internal one.

This is not guidance. It’s governance.

How Visa monitors performance

VAMP operates continuously, using defined thresholds to evaluate merchant activity across your portfolio. Visa tracks fraud and dispute ratios over time. When thresholds are exceeded, merchants, and their providers, are placed into formal monitoring programs with required corrective action. The challenge is that many organizations still rely on manual fraud workflows*, which makes it harder to prevent sustained ratio drift before Visa escalates.

Monitoring is automated and always on.

Threshold breaches trigger mandatory escalation, not warnings.

Corrective action is required within fixed timelines.

Remediation must be documented and verified.

Inaction increases scrutiny and exposure.

You don’t opt into monitoring, you trigger it.

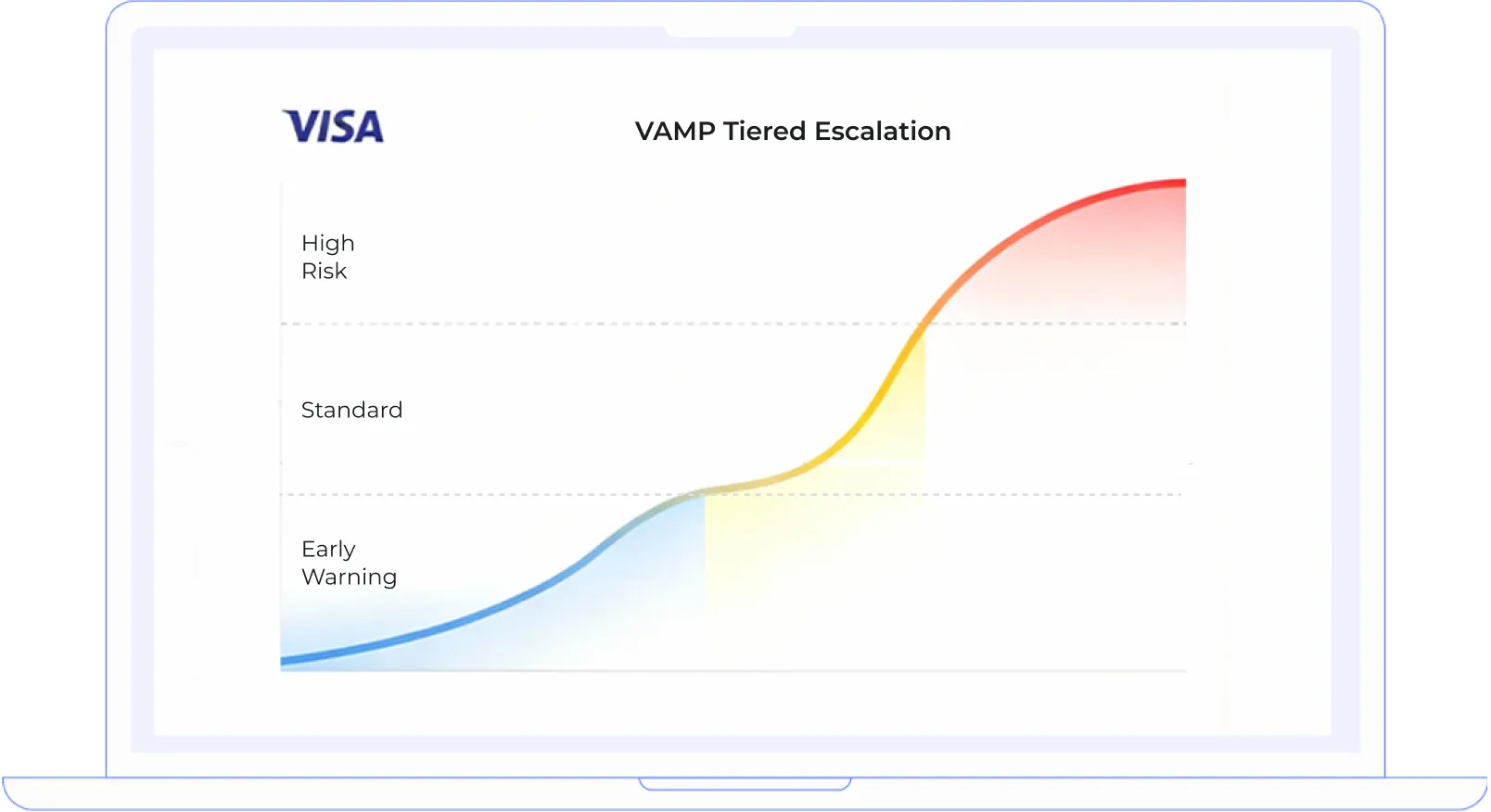

Escalation is tiered and cumulative

VAMP is structured to intensify oversight as risk persists. Visa applies different monitoring programs based on severity, each introducing stricter requirements and greater consequences. Meanwhile, fraud friction becomes a conversion problem, fraud prevention controls increase churn at 59% of U.S. merchants*, creating pressure between protection and approvals.

Early warning programs signal emerging risk.

Standard monitoring introduces formal remediation.

High risk programs carry the greatest restrictions and penalties.

Requirements increase at each level, not reset.

Time in program matters as much as ratios.

Once escalated, the path only moves forward, or out.

The impact on your merchants and your business

VAMP outcomes impact merchant viability and portfolio stability. When fraud and disputes rise, merchants face restrictions that hit resellers. The loss starts earlier through false declines, averaging 1.51% of ecommerce sales*, reducing conversion and value.

Mandatory remediation plans disrupt operations.

Processing restrictions reduce revenue and volume.

Increased reporting creates ongoing overhead.

Severe cases result in account termination.

Portfolio risk affects approvals and future growth.

Merchant performance is now a business liability.

Visa Acquirer Monitoring Program (VAMP) Fee Schedule

Identification Level

VAMP ratio threshold

Enforcement fee

when fees start

Acquirer, Early Warning

Below 0.3%

None

Not applicable

Acquirer, Above Standard

0.3% to below 0.5%

$4/ Count

Jan 1, 2026

Acquirer, Excessive

0.5% or higher

$8/ Count

Oct 1, 2025

Merchant, Excessive

1.5% or higher in 2025, 0.9% in 2026

$8/ Count

Oct 1, 2025

VAMP combines fraud and dispute activity into a single ratio, with fees assessed per fraudulent or disputed transaction and passed through the acquirer.

Fraud prevention can’t save you, but Zero Risk Processing can.

IoniaPay’s proprietary F3 software solution directly addresses the core risk areas enforced by the Visa Acquirer Monitoring Program by eliminating fraud and dispute exposure before transactions ever reach authorization. F3 uses real time, multi factor identity validation to confirm true cardholder ownership and match transactions to legitimate customers, blocking only high risk attempts upstream. This stops fraud before it reaches the processor and shifts liability away from merchants and providers.

As a result, F3 reduces the fraud rates and dispute ratios that trigger VAMP monitoring, making merchants less likely to escalate into early warning, standard, or high-risk programs. Resellers also reduce the remediation, documentation, and operational burden that monitoring creates. This isn’t fraud prevention. This is fraud elimination, and that is Zero Risk Processing.

Additional resources

Becoming a partner is easy!

Join the revolution that is changing how the world moves money and eliminates fraud.

Become an IoniaPay partner and join a team of resellers and referral partners that are leading changes in Fintech that are long overdue. Be part of the experience and witness the biggest change in payment processing since, well... the credit card.

Become a Partner

*Visa® Disclaimer:

Visa is a registered trademark of Visa International Service Association.

*Legal:

This material is provided for educational purposes only and does not replace official card network rules. Subject to the F3 Addendum, IoniaPay does not assume any liability and does not guarantee fraud prevention or detection outcomes. All results and performance metrics are contingent upon proper system configuration, adherence to network rules, and ongoing compliance with applicable operational requirements.

*Citations:

LexisNexis® Risk Solutions. (2025). The True Cost of Fraud™ Study, Ecommerce and Retail Report, US and Canada Edition. (Referenced: $5.13 per $1 fraud loss, 59% churn impact, and manual fraud workflow context.) Citation for false decline stat of 1.51%, Cybersource. (2024). False declines average 1.51% of ecommerce sales.